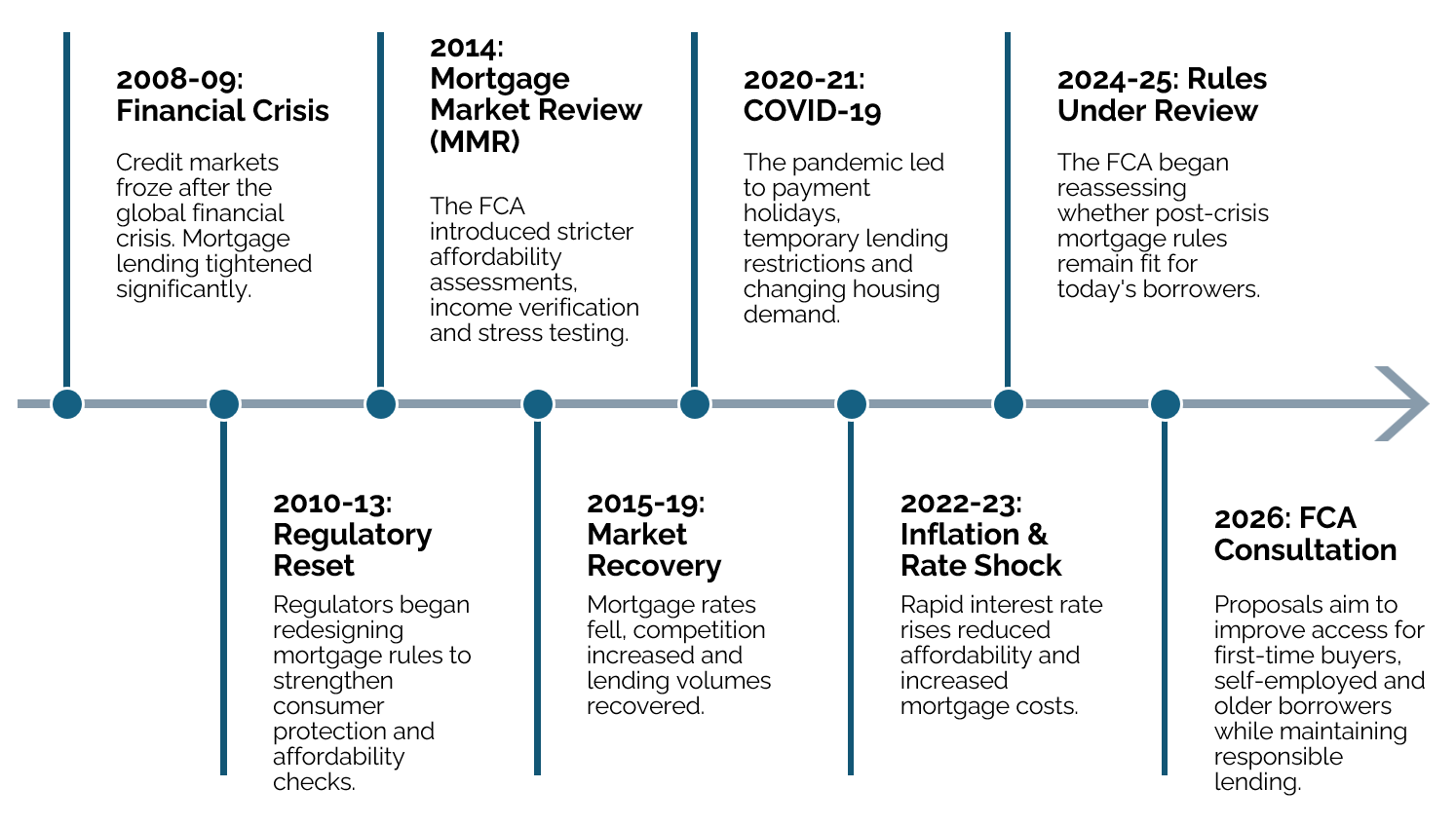

Last week, the FCA published a significant new consultation on mortgage lending, signalling what could become one of the biggest shifts in UK mortgage regulation since the Mortgage Market Review reforms introduced following the financial crisis.

From crisis rules to modern realities

Over the last 18 years, the UK mortgage market has moved from crisis and regulatory reform to resilience and maturity. Through CP26/18: Mortgage rule review – supporting first-time buyers and underserved consumers, the FCA is now asking whether rules designed to protect the market can also be adapted to improve access to it.

To some, these proposals may appear to present a return to pre-2008 thinking. But at Square 4, we think today’s discussion takes place against a backdrop of a changed society, the introduction of the Consumer Duty and far more sophisticated affordability assessments than existed during the financial crisis. The regulatory architecture is fundamentally different, and that matters.

What the FCA is actually saying

At the heart of the consultation is a straightforward acknowledgement: the market has changed, and the rules haven’t always kept pace.

Borrowers are increasingly extending their working lives, with many expecting to work later in life; they are earning income in different ways, and some are following less traditional career paths than when many of today’s mortgage rules were written. The FCA’s key proposals reflect this:

- Greater access for first-time buyers – The FCA believes some current practices (for example, the application of highly conservative assumptions) may be unnecessarily restricting access to home ownership, even where borrowers can comfortably afford repayments.

- Better outcomes for self-employed and non-traditional workers – Employment patterns in UK society have evolved and now:

- Approximately 4.3 million people in the UK are self-employed

- Second jobs have risen to around 1.3 million

- Around 1 million workers in the UK are estimated to be on zero-hours contracts, representing roughly 3% of the workforce.

With that in mind, the FCA wants lending assessments to better reflect these realities.

- Recognition that people are retiring later – the UK has an ageing population, with later retirement and changing career patterns becoming more common in today’s society. With this in mind, the regulator is proposing greater flexibility when assessing older borrowers and later-life income, rather than arbitrary rules on age alone.

- A more nuanced approach to affordability – Rather than relying on rigid affordability rules or automatic exclusions, the FCA is encouraging lenders to take a broader and holistic view of a borrower’s overall financial circumstances, which is reasonable and proportionate.

This is not a relaxation of responsible lending

It is worth being direct on this point. The consultation does not signal a loosening of consumer protections. Borrowers will still need to demonstrate they can afford and sustain their mortgage. Consumer Duty obligations will remain firmly in place, and lenders will remain responsible for robust affordability assessments and good customer outcomes.

Why the compliance question is the more interesting one

Much of the coverage published has focused on what these proposals mean for borrowers. For firms, we believe that the more consequential question is: what happens when lenders are given greater discretion?

Greater flexibility in lending decisions does not reduce regulatory accountability; it increases it. Firms will need to demonstrate that decisions are consistent, well-governed and evidence-based.

In practice, that means:

- Stronger documentation of individual lending decisions

- Clear governance frameworks for exercising discretion

- Robust outcomes testing to evidence Consumer Duty compliance

- Oversight processes that can withstand regulatory scrutiny

The commercial opportunity is real. But so is the compliance challenge. Firms that ensure the right infrastructure now will be better placed to compete as the rules evolve.

The bottom line, and what firms should be doing now

The FCA’s direction of travel is clear: preserve the post-crisis protections, while enabling firms to serve a broader range of borrowers.

Mortgage firms that will benefit most are not those that move fastest, but those that move most carefully, investing in good governance arrangements, documentation and outcomes testing before discretion becomes the norm rather than the exception.

If your firm is considering how to respond to this consultation, now is the time to assess your affordability frameworks to ensure they are robust and proportionate, so that you are well placed for any changes that follow. You should ensure that your decision-making audit trails enable you to evidence robust affordability assessments and that you can demonstrate good customer outcomes throughout the customer journey.

How Square 4 can help

At Square 4, we work with firms to navigate these challenges through a combination of compliance advisory services, specialist interim resource, technology-driven outcomes testing and managed service solutions.

Our mission is to protect regulated firms and support them to grow and thrive, helping you to adapt to regulatory change while maintaining confidence in your controls, operations and customer outcomes.

Nicola Crump – Advisory Director