Background

In December 2025, the FCA published a range of publications which impact UK investment markets, including:

- Discussion paper 25/3: Expanding consumer access to investments: seeking views on what more the FCA can do to ensure its regulations help consumers take informed risks and equip them with the confidence to invest.

- A statement on Consumer Duty expectations for firms working together to manufacture products or services: clarifies how the Consumer Duty applies when multiple firms work together to manufacture a product or service. The statement aims to give firms more clarity on supervisory expectations, greater confidence in applying the rules proportionately and to address areas where firms have interpreted the requirements more broadly than intended.

- Policy Statement 25/20: Supporting Informed Decision Making: Final Rules for Consumer Composite Investments: sets out the FCA’s final rules for Consumer Composite Investments (CCIs), introducing a more flexible, consumer-centric product information regime with standardised core content, greater design freedom for firms, and an 18-month implementation period before full entry into force.

The final rules for the CCI regime introduce a UK-specific disclosure framework for retail investors. Legislation in November 2024 set out the regulatory perimeter, replacing the PRIIPs KID and UCITS KIID requirements and bringing them onshore to the UK. Following consultations in December 2024 and April 2025, the FCA has now finalised the rules for firms undertaking designated CCI activities. The regime began on 6 April 2026, marking the start of a transition period during which manufacturers can choose to produce new product summaries while continuing to use existing disclosure documents. Full compliance will be required by 8 June 2027, with firms expected to use the transition period to prepare systems, processes and disclosures for implementation.

What is changing and why?

The FCA is replacing the PRIIPs KID and UCITS KIID with a simpler, more flexible retail disclosure regime for investment products, underpinned by the Consumer Duty. Feedback from consultations has shown that the existing frameworks have not always enabled retail investors to make well-informed decisions, relying instead on rigid templates and prescriptive disclosures that often result in technical, box-ticking documents which are difficult for consumers to understand.

Under the new CCI regime, each product will have a single UK-specific product summary, replacing separate PRIIPs KIDs and UCITS KIIDs and providing retail investors with one clear, consistent source of key information. The regime addresses previous shortcomings by focusing on the information consumers actually need, presented clearly and at the right time. Underpinned by the Consumer Duty, it removes excessive templating, allows firms to communicate flexibly, creatively, and retains standardisation only where it supports meaningful comparison. The overall aim is to demystify investing, improve understanding of costs, risks, returns, and give retail investors greater confidence to participate in long-term investing.

The CCI regime forms part of a broader push to strengthen the UK retail investment culture, aligning with the FCA’s Advice Guidance Boundary Review, which aims to improve how consumers access support and financial advice on pensions and investments, and the Government’s Financial Services Growth and Competitiveness strategy to boost participation and channel savings into productive capital markets.

When does it start?

The CCI disclosure regime will begin with an optional transition period from 6 April 2026, when the underlying legislation comes into force. From this date, manufacturers can choose either to adopt the new CCI product summary or continue using their existing disclosure documents, such as PRIIPs KIDs or UCITS KIIDs. This transitional flexibility applies to all manufacturers, including those of Overseas Funds Regime (OFR) schemes. The CCI regime will apply in full from 8 June 2027, when the new rules become mandatory.

Scope and applicability

The CCI regime applies to any firm that manufactures or distributes a CCI to a UK retail investor. Manufacturers are those who create, develop, design, issue, manage, or operate a CCI, while distributors are those who offer, advise on, or sell a CCI or provide related investment services. Firms engaging in either role must comply with the FCA’s retail disclosure rules, including operators of Overseas Funds Regime (OFR) recognised schemes.

The regime covers products where returns depend on the performance or value of underlying or reference assets, including open-ended funds, closed-ended funds, structured products and deposits, contracts for difference (CFDs), insurance-based investment products (IBIPs), and other complex products such as derivatives. Products explicitly excluded include vanilla corporate bonds, pension products, and pure protection insurance contracts.

Broadly similar to the former PRIIPs scope, the CCI regime consolidates all products into a single UK framework, replacing KIDs/KIIDs with a product summary, shifting to activity-based terminology (manufacture, distribution, advice), and aligning language with Consumer Duty principles.

Obligations on manufacturers

Manufacturers must produce a consumer-friendly product summary that provides retail investors with clear, comparable key information about costs, risks, and returns, as well as past performance. There is no fixed template or page limit, but the summary must be clear, fair, and easy for investors to understand, in line with the Consumer Duty. Mandatory core disclosures include:

- How the product works

- Risks (including a 1–10 risk score)

- Costs and charges

- Past performance

- Exit terms and recommended holding period

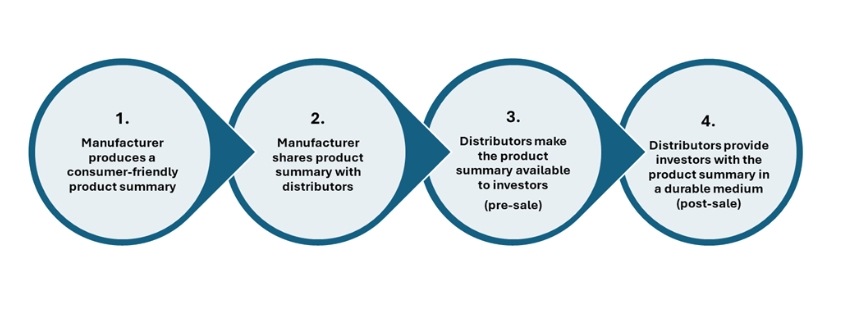

The product summary must be reviewed at least annually, updated following material changes, and shared with distributors before the product is sold. Where a product has multiple manufacturers, responsibilities must be set out in writing, with one firm able to take overall responsibility (for example, the AIFM for listed funds).

Obligations on distributors

Distributors must make the manufacturer’s product summary available to retail investors at an appropriate point in the customer journey and highlight key information to help consumers make effective and informed investment decisions. This includes drawing attention to risks, costs, performance, and relevant warnings.

Distributors have flexibility to provide this information in innovative ways that support consumer understanding, such as interactive digital tools or layered disclosures. They are not required to assess whether the summary meets each investor’s individual needs or to modify or rewrite it, unless it is materially misleading. The product summary must be available before the investor commits, and a copy should be provided in a durable medium (e.g., PDF) at or shortly after the sale.

Example Components of a Consumer-Friendly Product Summary (CCI)

While the FCA does not provide a standard template, manufacturers are required to create a consumer-friendly product summary containing key information about the investment. In practice, a summary might include the following components:

- Product overview

- Name of the CCI product and unique identifier

- Type of CII and its main features (including investment objectives and strategy)

- Recommended holding period (if relevant), exit terms, and any relevant redress information

- Risk and return

- Clear explanation of the main risks associated with the product

- CCI risk/return score on a 1–10 scale (with a brief narrative to explain what this means for investors)

- Product-specific risk scores for certain high-risk CCIs (e.g., VCTs, EISs, leveraged or derivative products) to reflect their inherent risks.

- Costs and charges

- Summary of all direct and indirect costs, including ongoing, one-off, and transaction fees

- Any performance-related charges clearly highlighted

- Past performance

- Past performance shown on a standardised line graph for up to 10 years (or the available period) and based on an initial investment of £10,000 (or equivalent in non-sterling currency).

- Depending on the CCI, include relevant benchmark information.

Next Steps

The FCA will support firms during the 18-month implementation period and monitor the regime’s effectiveness once live, focusing on the readability, accessibility and consumer understanding of product information. Firms should confirm their role as manufacturer or distributor and identify in-scope products, prepare CCI documentation, and review systems, processes, and governance to ensure accurate and maintainable disclosures. Policies and distribution arrangements should be updated to align with Consumer Duty and financial promotion requirements, and firms should undertake readability and accessibility testing, as well as consumer-focused checks such as focus groups or comprehension surveys, to evidence that product information supports positive consumer outcomes. The key risk for firms is producing disclosures that technically comply but fail Consumer Duty.

How can Square 4 help?

Square 4 supports firms in navigating the new Consumer Composite Investments (CCI) regime, helping translate regulatory expectations into clear, consumer-focused, and compliant disclosure practices. Our team brings deep experience across Consumer Duty, product governance, and retail investment compliance, assisting manufacturers and distributors to design, test, and implement product summaries that are readable, accessible, and fit for purpose.

We help firms:

- Map roles and products in scope: confirming manufacturer/distributor responsibilities and which products fall under the CCI regime.

- Develop transition plans: aligning timelines with existing KID/KIID review cycles and incorporating the design, testing, and finalisation of CCI documentation.

- Assess systems, data, and governance: ensuring processes to produce, maintain, and share core disclosure information are robust, updating controls, governance, and oversight arrangements as necessary.

- Test consumer understanding: using readability tools, accessibility reviews, focus groups, and surveys to evidence that product information is clear, fair, and supports informed decision-making.

- Align policies and distribution arrangements: including Consumer Duty and financial promotion compliance.

If you would like to discuss how we can support your business further, please get in touch:

- Simon Goryl - Advisory Director (Wealth): sgoryl@square4.com

- Luke Wootton - Client Relationship Director (Wealth): lwootton@square4.com

Alice Buckley

Consultant